Families bear the brunt of first home buyer crisis

Parents are risking their own financial well-being to help adult children buy a first home

- One in five (19.1%) of first home buyers nationally rely on a cash gift from family members – a figure that rises to 30.7% of first home buyers in Queensland, and falls to 1.9% among New South Wales first home buyers.

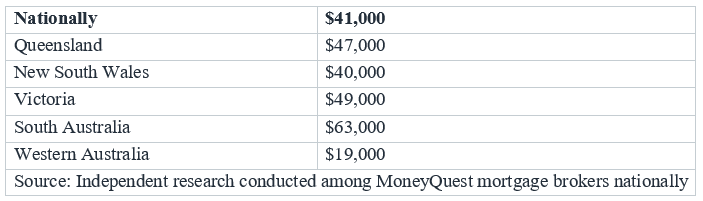

- Parents offering financial support are gifting, on average, $41,000 to help their adult children buy a first home.

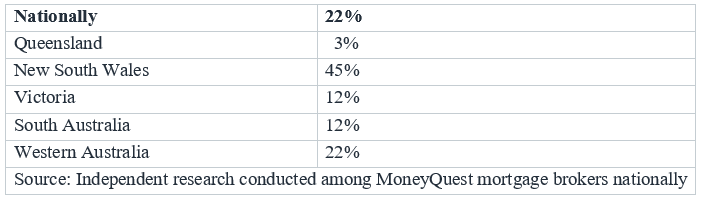

- One in four (22%) first home buyers rely on the support of a guarantor – usually a parent.

- 13% of first home buyers are opting to buy an investment property while living at home.

- Only 3% of first home buyers nationally are “rentvesting” – purchasing a rental property while renting themselves.

Melbourne, 8th February 2017: Research by leading national mortgage broking group MoneyQuest reveals that declining housing affordability is having a multi-generational impact as first home buyers increasingly rely on the financial support of parents to secure their first home.

The nature of parental support varies widely between states. Nationally, one in five (19.1%) first home buyers receive a cash gift from parents to purchase a home, a figure that rises to 30.7% of first home buyers in Queensland. By contrast, only 1.7% of first home buyers in New South Wales receive a cash handout from parents.

Proportion of first home buyers receiving a financial helping hand from parents:

Average Cash Gift of $41,000

Among first home buyers who have received financial support from family members, the average cash gift nationally is $41,000. This figures rises to $63,000 among South Australian first home buyers – the most generous handout nationally.

Average sum of sum gifted to first home buyers by family members:

Michael Russell, Managing Director of MoneyQuest says, “Declining housing affordability has seen first home buyer activity drop significantly, accounting for just 13.8 percent of new home loans at present, down from 18 percent ten years ago.”

“The fall in first home buyer numbers is rapidly becoming an intergenerational issue with older parents under pressure to gift tens of thousands of dollars to their adult children at a time when the Federal government is urging all Australians to provide for their own retirement,” said Michael Russell.

One in Four First Home Buyers Rely on a Guarantor

Nationally, almost one in four (22%) first home buyers are providing a guarantor to secure a home loan, a figure that rises to 45% of New South Wales first home buyers.

First home buyers relying on a guarantor:

Michael Russell notes, “Providing a guarantor can be a great option for first home buyers with a small deposit to enter the market, and on the face of it, agreeing to act as a guarantor offers a way for cash-strapped parents to support their adult child’s goal of home ownership. In New South Wales for instance, we see less than two percent of first home buyers receive a cash gift from parents, yet almost one in two New South Wales first home buyers are providing a guarantor for their loan.”

“Agreeing to be a guarantor is not a step to be taken lightly, especially among parents who are in or approaching retirement. It can severely limit the ability of the guarantor to secure credit for their own needs, and if the first home buyer defaults on the loan, the lender can turn to the guarantor to take over the loan repayments, something that could be financially disastrous for many older parents,” added Michael Russell.

One in Ten Buy as an Investor

MoneyQuest figures confirm that 13% of first home buyers nationally are opting out of buying an owner occupied home, and choosing to purchase an investment property while continuing to live at home. This strategy is most prevalent in New South Wales and Victoria where 24% and 20% of first home buyers respectively are investing in a rental property rather than buying a home to live in.

Nationally, only 3% of first home buyers are “rentvesting” – purchasing a rental property, while renting a place to live in themselves.

Michael Russell says, “The affordability crisis facing first home buyers brings with it serious collateral issues that now extend across several generations. If Federal and State governments continue to ignore the problem for much longer, Australia will face a massive intergenerational shift in property ownership that as a nation we are completely unprepared for.”

“Home ownership has long formed one of the nation’s key pillars of retirement, and as it stands, not only are younger generations struggling to achieve this goal, older Australians may be jeopardising their own financial well-being by giving their adult children desperately needed financial support to buy into the property market. The support of a home loan expert is vital for first home buyers to understand the options available to them, but more broadly the affordability crisis demands the urgent attention of politicians at both State and Federal level.” concluded Michael Russell.

About MoneyQuest

Established in 2007, MoneyQuest was founded with a clear goal – to make property ownership easy and rewarding for everyday Australians. MoneyQuest has over 40 offices across Australia helping thousands of families and investors build their financial future – from first home ownership right through to retirement. More information on MoneyQuest.

Money Quest Australia Pty Ltd, Australian Credit Licence 487823.

For more information:

Michael Russell

Managing Director

MoneyQuest

[email protected]

(03) 9583 6598

Disclaimer:

This article is written to provide a summary and general overview of the subject matter covered for your information only. Every effort has been made to ensure the information in the article is current, accurate and reliable. This article has been prepared without taking into account your objectives, personal circumstances, financial situation or needs. You should consider whether it is appropriate for your circumstances. You should seek your own independent legal, financial and taxation advice before acting or relying on any of the content contained in the articles and review any relevant Product Disclosure Statement (PDS), Terms and Conditions (T&C) or Financial Services Guide (FSG).

Please consult your financial advisor, solicitor or accountant before acting on information contained in this publication.

Proudly Part Of

The Money Quest Group (MQG) is one of Australia's leading boutique mortgage broking businesses, with a network of more than 600 brokers nationwide. Known for their exuberant culture and superior support, MQG provides brokers access to a range of financial products from more than 60 lending institutions and suppliers, and exclusive access to in-house benefits and services.

© 2017-2025 MoneyQuest Australia Pty Ltd, Australian Credit Licence 487823