Understanding Lenders Mortgage Insurance (LMI).

When you’re on the journey to buying a home, you’ll encounter various costs and terms that may seem confusing at first. One of these terms is Lenders Mortgage Insurance (LMI). While it’s often misunderstood, LMI plays a crucial role in helping many Australians achieve their dream of home ownership sooner. Let’s break it down.

What is Lenders Mortgage Insurance?

Lenders Mortgage Insurance is a one-time premium designed to protect the lender if a borrower is unable to meet their home loan repayments and defaults on the loan. Importantly, LMI protects the lender, not the borrower. However, it can benefit borrowers indirectly by enabling them to secure a loan with a lower deposit.

Typically, lenders require a 20% deposit of the property’s purchase price to approve a loan without LMI. If you’re unable to save that amount, you can still get a loan—but you’ll likely need to pay LMI.

How is LMI calculated?

The cost of LMI depends on several factors, including:

- The size of your deposit.

- The loan amount.

- The loan-to-value ratio (LVR)

- The lender you’re working with

LMI is a one off fee, but it can often your loan repayment amount if you can’t pay it upfront.

How does LMI work?

LMI is calculated based on the size of your loan and the percentage of your deposit (Loan-to-Value Ratio, or LVR). The higher the LVR, the higher the LMI premium.

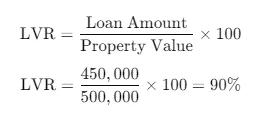

For example, let’s say you want to buy a property worth $500,000 but only have a $50,000 deposit (10%). Your LVR would be:

In this case, because your deposit is less than 20% of the property’s value, LMI would apply. The exact cost depends on the lender and insurer, but for a 90% LVR, it might be around $8,000 to $12,000.

How is LMI paid?

LMI can be paid upfront as a lump sum at settlement or capitalised (added to your loan amount). Let’s consider the capitalised option with our previous example. If your LMI premium is $10,000, and you add this to your $450,000 loan:

![]()

In this case, $450,000 + $10,000 = $460,000

This means your repayments will be calculated based on a $460,000 loan rather than $450,000.

Benefits of LMI.

1. Enter the property market sooner:

LMI allows you to buy a home with a smaller deposit, which can be especially helpful in a rising market.

2. Flexible deposit options:

Moving often means a flood of small purchases, tools, fittings, and/or furniture. Keep digital receipts in one place. If you’re an investor or have a home office, some costs may be deductible.

3. More lending opportunities:

LMI provides lenders with added security, making it easier for borrowers with smaller deposits to get approved.

Tips to Minimise LMI Costs.

1. Save a larger deposit:

Increasing your deposit reduces your LVR and may lower or eliminate your LMI costs.

2. Consider a Guarantor:

Some lenders allow a family member to guarantee part of your loan, which can help you avoid LMI.

3. Shop Around:

Lenders and insurers calculate LMI differently. A mortgage broker can help you compare options and find the best deal.

Is LMI Tax-Deductible?

For owner-occupiers, LMI is not tax-deductible. However, if you’re purchasing an investment property, you may be able to claim LMI as a tax deduction over a period of five years.

Final Thoughts

LMI is an important tool that makes home ownership accessible to more Australians. While it’s an additional cost, it can be the key to buying your home sooner rather than later. Working with a knowledgeable mortgage broker ensures you understand your options and make informed decisions about your home loan.

If you’re unsure how LMI affects your situation, contact us today. We’re here to guide you through every step of your home-buying journey.

Disclaimer:

This article is written to provide a summary and general overview of the subject matter covered for your information only. Every effort has been made to ensure the information in the article is current, accurate and reliable. This article has been prepared without taking into account your objectives, personal circumstances, financial situation or needs. You should consider whether it is appropriate for your circumstances. You should seek your own independent legal, financial and taxation advice before acting or relying on any of the content contained in the articles and review any relevant Product Disclosure Statement (PDS), Terms and Conditions (T&C) or Financial Services Guide (FSG).

Please consult your financial advisor, solicitor or accountant before acting on information contained in this publication.

Proudly Part Of

The Money Quest Group (MQG) is one of Australia's leading boutique mortgage broking businesses, with a network of more than 600 brokers nationwide. Known for their exuberant culture and superior support, MQG provides brokers access to a range of financial products from more than 60 lending institutions and suppliers, and exclusive access to in-house benefits and services.

© 2017-2025 MoneyQuest Australia Pty Ltd, Australian Credit Licence 487823